R: Markov Chain Wikipedia Example

Over the weekend I’ve been reading about Markov Chains and I thought it’d be an interesting exercise for me to translate Wikipedia’s example into R code.

But first a definition:

A Markov chain is a random process that undergoes transitions from one state to another on a state space. It is required to possess a property that is usually characterized as "memoryless": the probability distribution of the next state depends only on the current state and not on the sequence of events that preceded it.

that 'random process' could be moves in a Monopoly game, the next word in a sentence or, as in Wikipedia’s example, the next state of the Stock Market.

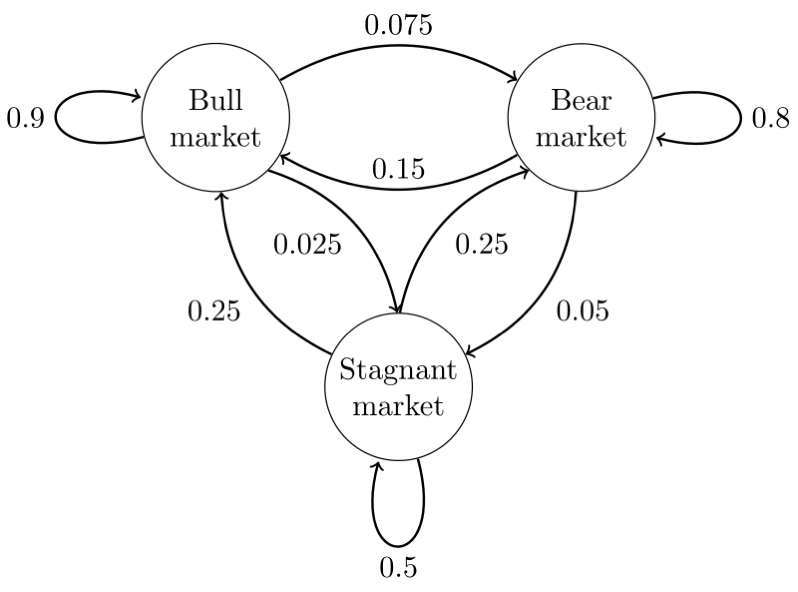

The diagram below shows the probabilities of transitioning between the various states:

e.g. if we’re in a Bull Market the probability of the state of the market next week being a Bull Market is 0.9, a Bear Market is 0.075 and a Stagnant Market is 0.025.

We can model the various transition probabilities as a matrix:

M = matrix(c(0.9, 0.075, 0.025, 0.15, 0.8, 0.05, 0.25, 0.25, 0.5),

nrow = 3,

ncol = 3,

byrow = TRUE)

> M

[,1] [,2] [,3]

[1,] 0.90 0.075 0.025

[2,] 0.15 0.800 0.050

[3,] 0.25 0.250 0.500Rows/Cols 1-3 are Bull, Bear, Stagnant respectively.

Now let’s say we start with a Bear market and want to find the probability of each state in 3 weeks time.

We can do this is by multiplying our probability/transition matrix by itself 3 times and then multiplying the result by a vector representing the initial Bear market state.

threeIterations = (M %*% M %*% M)

> threeIterations

> threeIterations

[,1] [,2] [,3]

[1,] 0.7745 0.17875 0.04675

[2,] 0.3575 0.56825 0.07425

[3,] 0.4675 0.37125 0.16125

> c(0,1,0) %*% threeIterations

[,1] [,2] [,3]

[1,] 0.3575 0.56825 0.07425So we have a 56.825% chance of still being in a Bear Market, 35.75% chance that we’re now in a Bull Market and only a 7.425% chance of being in a stagnant market.

I found it a bit annoying having to type '%*% M' multiple times but luckily the expm library allows us to apply a Matrix power operation:

install.packages("expm")

library(expm)

> M %^% 3

[,1] [,2] [,3]

[1,] 0.7745 0.17875 0.04675

[2,] 0.3575 0.56825 0.07425

[3,] 0.4675 0.37125 0.16125The nice thing about this function is that we can now easily see where the stock market will trend towards over a large number of weeks:

> M %^% 100

[,1] [,2] [,3]

[1,] 0.625 0.3125 0.0625

[2,] 0.625 0.3125 0.0625

[3,] 0.625 0.3125 0.0625i.e. 62.5% of weeks we will be in a bull market, 31.25% of weeks will be in a bear market and 6.25% of weeks will be stagnant,

About the author

I'm currently working on short form content at ClickHouse. I publish short 5 minute videos showing how to solve data problems on YouTube @LearnDataWithMark. I previously worked on graph analytics at Neo4j, where I also co-authored the O'Reilly Graph Algorithms Book with Amy Hodler.